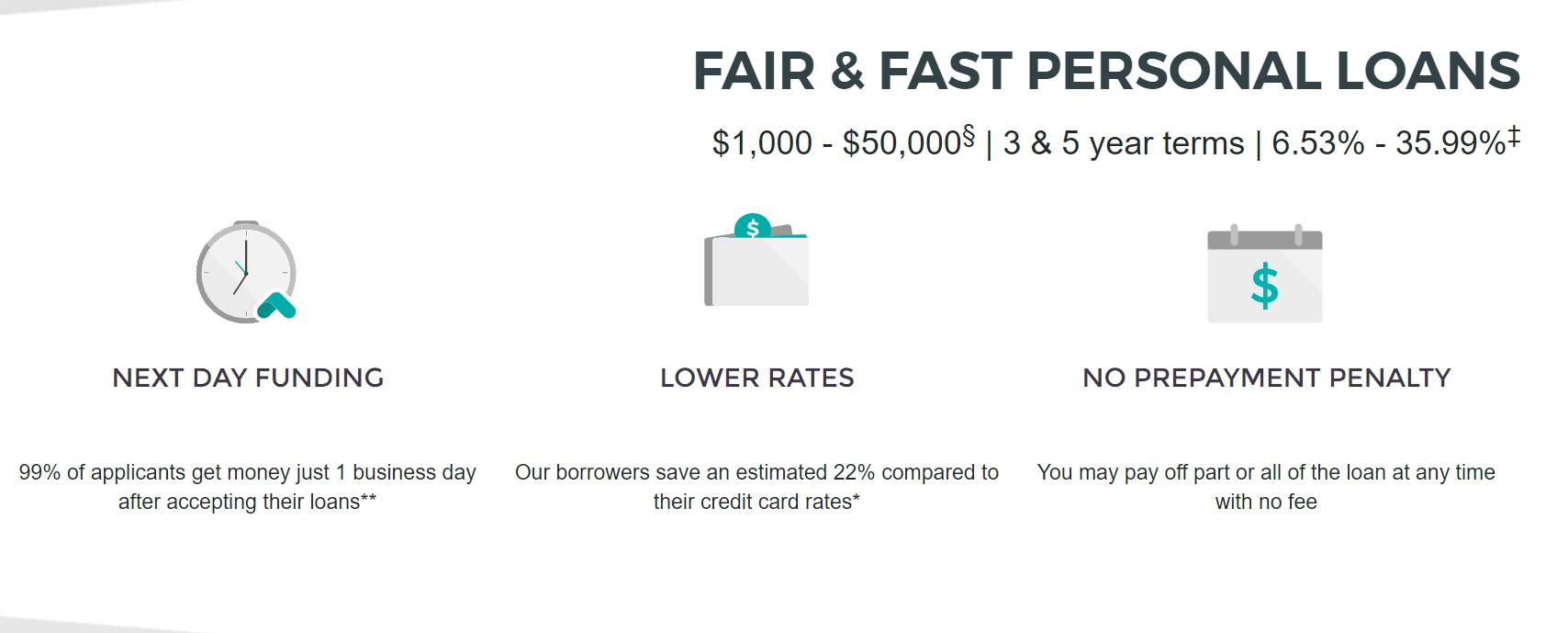

Consolidating debt has many benefits. Consolidating debt can lower interest rates, improve credit scores, and simplify your repayments. It is important that you understand the cons. This article will explore the advantages and disadvantages of debt consolidation. A consolidation loan for debt can lower interest rates and increase monthly payments.

Lower-interest debt consolidation reduces interest charges

If you're a victim of credit card debt, a lower-interest debt consolidation loan can help you pay off your bills faster. This is a great way of reducing the amount of bills you have accrued since the recent financial crisis. These tips will make debt consolidation easier for you.

Consolidating debt at lower interest can reduce interest charges. This is done by combining all your debts in one low-interest loans. This will allow you to free up your credit and stop collection calls. Applying for a new mortgage will temporarily lower your credit score. Consolidating debt will improve your credit score over the long-term if you continue to make your payments and pay down your credit cards.

It can help you improve your credit score

If you're in debt, you may be wondering whether debt consolidation can improve your credit score. The answer depends on how you approach debt consolidation. There are many options. One is to take out a new credit card or loan. This lowers your score. Others involve negotiating for a reduced payment. You will need to consider your credit score, credit utilization ratio and payment history before deciding if debt consolidation is right for you.

Your payment history can affect your credit score. That is why it is important that you pay on time. The initial credit score of a debt consolidation loan will be lower, but the new monthly installment will be easier. Because your payment history makes up 35 percent of your credit score, paying on time can improve your credit score.

It can streamline repayment

If you want to make your payments easier, debt consolidation may be a good choice. It can help people reduce their monthly payments by combining all their debts into one loan or credit card. They then use the funds to pay off any outstanding balances. This can make repayment easier, and it improves their credit score.

Online application for debt consolidation loans can be made through a bank or credit card union. Funds may be available within a few days of approval. This money can be used for your existing debts. The lender can also pay them off.

It can help you increase your monthly payments

You might be wondering if consolidation is right for your needs. There are many benefits to debt consolidation, including a lower monthly repayment and a lower rate of interest. By comparing different loan offers, you can determine which option is best for you. A debt consolidation service will also help you choose the repayment period that best suits your financial situation. While shorter repayment terms may result in higher monthly payments, they can also save you more over the life of your loan. Consolidation also works well as a debt management tool, because it allows for better planning and reduces monthly repayments.

Although debt consolidation may seem like a good solution for you, there are some drawbacks as well. High interest rates are the main problem. You can pay your debt faster with debt consolidation. It will mean that you only have one lender.

It can raise your interest-rate

Although a debt consolidation loan has the advantage of lower monthly payments, this convenience can come at a price. Prepayment penalties and origination charges are common for debt consolidation loans. These fees can decrease the savings due to the lower interest rates. Lenders typically charge these fees in the range of one percent to five percent of the total loan amount. Before you apply to consolidate debt, be sure to review all terms and conditions.

In the event that you do not pay your bills in time, credit card companies could raise your interest rate. While debt consolidation loans will often consolidate your credit card balances into a single payment, they can damage your credit score. It is important to plan your monthly budget well and avoid missing any payments by using autopay or other payment methods. It is important to speak with your lender regarding any circumstances that could cause you miss a payment.

FAQ

How much debt can you take on?

It is vital to realize that you can never have too much money. You will eventually run out money if you spend more than your income. Because savings take time to grow, it is best to limit your spending. So when you find yourself running low on funds, make sure you cut back on spending.

But how much should you live with? There isn't an exact number that applies to everyone, but the general rule is that you should aim to live within 10% of your income. This will ensure that you don't go bankrupt even after years of saving.

This means that if you make $10,000 yearly, you shouldn't spend more than $1,000 monthly. If you make $20,000, you should' t spend more than $2,000 per month. And if you make $50,000, you shouldn't spend more than $5,000 per month.

It's important to pay off any debts as soon and as quickly as you can. This includes student loans, credit card debts, car payments, and credit card bill. When these are paid off you'll have money left to save.

You should consider where you plan to put your excess income. If you choose to invest your money in bonds or stocks, you may lose it if the stock exchange falls. You can still expect interest to accrue if your money is saved.

Let's suppose, for instance, that you put aside $100 every week to save. It would add up towards $500 over five-years. At the end of six years, you'd have $1,000 saved. You would have $3,000 in your bank account within eight years. When you turn ten, you will have almost $13,000 in savings.

At the end of 15 years, you'll have nearly $40,000 in savings. That's quite impressive. If you had made the same investment in the stock markets during the same time, you would have earned interest. Instead of $40,000 in savings, you would have more than 57,000.

It's crucial to learn how you can manage your finances effectively. Otherwise, you might wind up with far more money than you planned.

Which side hustles have the highest potential to be profitable?

Side hustle is an industry term that refers to any additional income streams that supplement your main source.

Side hustles provide extra income for fun activities and bills.

Side hustles may also allow you to save more money for retirement and give you more flexibility in your work schedule. They can even help you increase your earning potential.

There are two types. Online businesses, such as blogs, ecommerce stores and freelancing, are passive side hustles. Side hustles that are active include tutoring, dog walking, and selling products on eBay.

Side hustles are smart and can fit into your life. Start a fitness company if you are passionate about working out. You may be interested in becoming a freelance landscaper if your passion is spending time outdoors.

You can find side hustles anywhere. Consider side hustles where you spend your time already, such as volunteering or teaching classes.

One example is to open your own graphic design studio, if graphic design experience is something you have. Maybe you're a writer and want to become a ghostwriter.

Do your research before starting any side-business. If the opportunity arises, this will allow you to be prepared to seize it.

Side hustles can't be just about making a living. Side hustles are about creating wealth and freedom.

There are so many opportunities to make money that you don't have to give up, so why not get one?

What side hustles will be the most profitable in 2022

To create value for another person is the best way to make today's money. If you do this well the money will follow.

It may seem strange, but your creations of value have been going on since the day you were born. When you were a baby, you sucked your mommy's breast milk and she gave you life. You made your life easier by learning to walk.

Giving value to your friends and family will help you make more. The truth is that the more you give, you will receive more.

Everybody uses value creation every single day, without realizing it. Whether you're cooking dinner for your family, driving your kids to school, taking out the trash, or simply paying the bills, you're constantly creating value.

In reality, Earth has nearly 7 Billion people. This means that every person creates a tremendous amount of value each day. Even if you create only $1 per hour of value, you would be creating $7,000,000 a year.

It means that if there were ten ways to add $100 to the lives of someone every week, you'd make $700,000.000 extra per year. That's a huge increase in your earning potential than what you get from working full-time.

Let's suppose you wanted to increase that number by doubling it. Let's suppose you find 20 ways to increase $200 each month in someone's life. Not only would you make an additional $14.4million dollars per year, but you'd also become extremely wealthy.

Every day, there are millions upon millions of opportunities to create wealth. This includes selling information, products and services.

Even though we spend much of our time focused on jobs, careers, and income streams, these are merely tools that help us accomplish our goals. Helping others to achieve their goals is the ultimate goal.

Create value to make it easier for yourself and others. Start by downloading my free guide, How to Create Value and Get Paid for It.

What's the difference between passive income vs active income?

Passive income refers to making money while not working. Active income requires hard work and effort.

When you make value for others, that is called active income. Earn money by providing a service or product to someone. For example, selling products online, writing an ebook, creating a website, advertising your business, etc.

Passive income allows you to be more productive while making money. Most people don't want to work for themselves. They choose to make passive income and invest their time and energy.

The problem with passive income is that it doesn't last forever. You might run out of money if you don't generate passive income in the right time.

It is possible to burn out if your passive income efforts are too intense. It is best to get started right away. If you wait to start earning passive income, you might miss out opportunities to maximize the potential of your earnings.

There are three types to passive income streams.

-

There are many options for businesses: You can own a franchise, start a blog, become a freelancer or rent out real estate.

-

Investments - these include stocks and bonds, mutual funds, and ETFs

-

Real estate - This includes buying and flipping homes, renting properties, and investing in commercial real property.

What is personal finances?

Personal finance is the art of managing your own finances to help you achieve your financial goals. This means understanding where your money goes and what you can afford. And, it also requires balancing the needs of your wants against your financial goals.

Learning these skills will make you financially independent. You won't need to rely on anyone else for your needs. You don't need to worry about monthly rent and utility bills.

Not only will it help you to get ahead, but also how to manage your money. It makes you happier. You will feel happier about your finances and be more satisfied with your life.

Who cares about personal finances? Everyone does! Personal finance is the most popular topic on the Internet. According to Google Trends, searches for "personal finance" increased by 1,600% between 2004 and 2014.

People use their smartphones today to manage their finances, compare prices and build wealth. They read blogs such this one, listen to podcasts about investing, and watch YouTube videos about personal financial planning.

In fact, according to Bankrate.com, Americans spend an average of four hours a day watching TV, listening to music, playing video games, surfing the Web, reading books, and talking with friends. Only two hours are left each day to do the rest of what is important.

If you are able to master personal finance, you will be able make the most of it.

Why is personal finance so important?

If you want to be successful, personal financial management is a must-have skill. We live in a world where money is tight, and we often have to make difficult decisions about how to spend our hard-earned cash.

So why should we wait to save money? What is the best thing to do with our time and energy?

Both yes and no. Yes, because most people feel guilty if they save money. Because the more money you earn the greater the opportunities to invest.

Focusing on the big picture will help you justify spending your money.

You must learn to control your emotions in order to be financially successful. Negative thoughts will keep you from having positive thoughts.

It is possible to have unrealistic expectations of how much you will accumulate. You don't know how to properly manage your finances.

After mastering these skills, it's time to learn how to budget.

Budgeting means putting aside a portion every month for future expenses. Planning will help you avoid unnecessary purchases and make sure you have enough money to pay your bills.

Now that you understand how to best allocate your resources, it is possible to start looking forward to a better financial future.

Statistics

- Mortgage rates hit 7.08%, Freddie Mac says Most Popular (marketwatch.com)

- Etsy boasted about 96 million active buyers and grossed over $13.5 billion in merchandise sales in 2021, according to data from Statista. (nerdwallet.com)

- According to a June 2022 NerdWallet survey conducted online by The Harris Poll. (nerdwallet.com)

- U.S. stocks could rally another 25% now that Fed no longer has ‘back against the wall' in inflation fight (marketwatch.com)

- 4 in 5 Americans (80%) say they put off financial decisions, and 35% of those delaying those decisions say it's because they feel overwhelmed at the thought of them. (nerdwallet.com)

External Links

How To

How passive income can improve cash flow

It is possible to make money online with no hard work. Instead, passive income can be made from your home.

Perhaps you have an existing business which could benefit from automation. If you are considering starting your own business, automating parts can help you save money and increase productivity.

The more automated your business becomes, the more efficient it will become. This means you will be able to spend more time working on growing your business rather than running it.

A great way to automate tasks is to outsource them. Outsourcing allows you to focus on what matters most when running your business. By outsourcing a task you effectively delegate it to another party.

This allows you to focus on the essential aspects of your business, while having someone else take care of the details. Outsourcing helps you grow your business by removing the need to manage the small details.

You can also turn your hobby into an income stream by starting a side business. Using your skills and talents to create a product or service that can be sold online is another way to generate extra cash flow.

You might consider writing articles if you are a writer. You have many options for publishing your articles. These sites pay per article and allow you to make extra cash monthly.

It is possible to create videos. You can upload videos to YouTube and Vimeo via many platforms. Posting these videos will increase traffic to your social media pages and website.

Stocks and shares are another way to make some money. Stocks and shares are similar to real estate investments. Instead of receiving rent, dividends are earned.

They are included in your dividend when shares you buy are purchased. The size of the dividend you receive will depend on how many stocks you purchase.

If your shares are sold later, you can reinvest any profits back into purchasing more shares. You will keep receiving dividends for as long as you live.