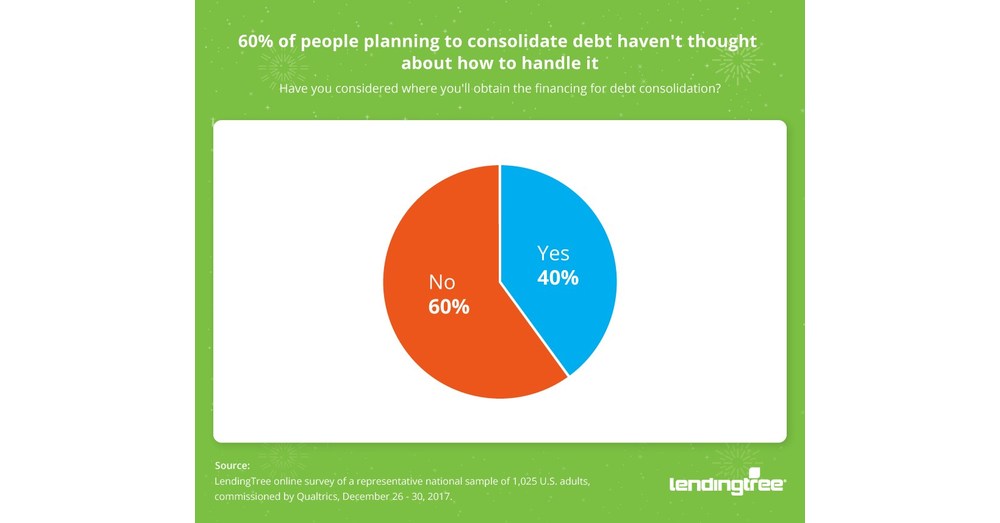

Although consolidation of medical debt sounds like a good solution, it may not be the best. For example, medical bills do not usually include interest and can often be combined with credit protections. A single payment may not offer the best value for money. If you can still benefit from one payment per month, it could be a good option.

Personal loan

Medical debt consolidation using a personal loan is a popular method to eliminate large medical bills. However, it is important to consider the risks of this option before applying for one. This option can make it easier to pay your bills and make it more affordable. But it can also make it more difficult. It could lead to late payments or even default if you fail to pay your bills on time. If you do this, you will lose the protections provided by federal and state law.

You have other options for consolidating medical debt. Personal loans for consolidation of medical debt are a great way to lower your monthly repayments and save interest. Lenders often allow soft credit checks to help you shop around. This will allow you to check interest rates without affecting credit scores. You can also apply at multiple lenders for the best deals.

Home equity loan

Home equity loans are a great way for consolidating medical debt. A home equity mortgage is a secured loan. This means that it is backed up by the house. A home equity loan can be applied for by most financial institutions and mortgage brokers. However, your original mortgage institution is the best place to apply.

HELOCs can be helpful in paying for medical expenses, but they are not without risks. First, a HELOC secured against your home can lead to your house being lost if you don't repay it and interest. You need to be aware of all possible options. Before applying for a HELOC you should speak with your doctor and negotiate a payment plan. A medical bill advocate may be a good option to reduce your bill. Then, shop around for the best HELOC lender. Before you agree to any lender, make sure that you have read and understood their terms and condition.

Transfer credit card to balance

Balance transfer credit cards are the best option for high-interest debt. You can get a lower interest rate with this type of card and simplify your financial life by making one low monthly payment instead of many. A good or excellent credit rating is necessary to receive balance transfer benefits. A secured credit card is another option if you don’t have a good credit score.

Low interest rates are the best balance transfer credit cards for consolidating medical debt. This will allow for you to make the monthly payment. A balance transfer credit card is a great way to save money on medical debt. However, you can damage your credit score by not making timely payments.

Negotiating with creditors

It is important to reach an agreement with the collection company if you have medical debt. You can have medical debts on your credit report for up seven years. It is crucial to get these debts resolved as soon as possible. There are many tactics you can use to negotiate with collections agencies, but the best way is to pay off all outstanding debts before you consider taking legal action. Another negotiating strategy is to ask for medical bill forgiveness. This can be a good option for low-income consumers who cannot afford a medical plan. Many hospitals also offer charity care to the uninsured and underinsured. For those who have certain assets and income requirements, government programs might also provide financial assistance.

If you need to lower or simplify the monthly payment of medical debt, consolidation can be an option. However, remember that medical debt consolidation is not a solution for all medical debts. Although it may be beneficial for the short-term, it could lead to higher monthly medical bills. You may also experience a decrease in your credit score. It is important to carefully assess your financial situation before you decide on a plan.

FAQ

How does a rich person make passive income?

There are two methods to make money online. One is to create great products/services that people love. This is called "earning” money.

A second option is to find a way of providing value to others without creating products. This is called "passive" income.

Let's assume you are the CEO of an app company. Your job is to create apps. You decide to give away the apps instead of making them available to users. Because you don't rely on paying customers, this is a great business model. Instead, you rely upon advertising revenue.

To help you pay your bills while you build your business, you may also be able to charge customers monthly.

This is the way that most internet entrepreneurs are able to make a living. Instead of making things, they focus on creating value for others.

How much debt are you allowed to take on?

It is vital to realize that you can never have too much money. You will eventually run out money if you spend more than your income. Because savings take time to grow, it is best to limit your spending. When you run out of money, reduce your spending.

But how much should you live with? Although there's no exact number that will work for everyone, it is a good rule to aim to live within 10%. You won't run out of money even after years spent saving.

This means that you shouldn't spend more money than $10,000 a year if your income is $10,000. If you make $20,000 per year, you shouldn't spend more then $2,000 each month. And if you make $50,000, you shouldn't spend more than $5,000 per month.

This is where the key is to pay off all debts as quickly and easily as possible. This includes credit card bills, student loans, car payments, etc. Once those are paid off, you'll have extra money left over to save.

It is best to consider whether or not you wish to invest any excess income. You may lose your money if the stock markets fall. If you save your money, interest will compound over time.

Let's suppose, for instance, that you put aside $100 every week to save. That would amount to $500 over five years. Over six years, that would amount to $1,000. You would have $3,000 in your bank account within eight years. By the time you reach ten years, you'd have nearly $13,000 in savings.

You'll have almost $40,000 sitting in your savings account at the end of fifteen years. This is quite remarkable. If you had made the same investment in the stock markets during the same time, you would have earned interest. Instead of $40,000, you'd now have more than $57,000.

This is why it is so important to understand how to properly manage your finances. You might end up with more money than you expected.

What is personal finance?

Personal finance is about managing your own money to achieve your goals at home and work. This includes understanding where your money is going and knowing how much you can afford. It also involves balancing what you want against what your needs are.

You can become financially independent by mastering these skills. That means you no longer have to depend on anyone for financial support. You can forget about worrying about rent, utilities, or any other monthly bills.

It's not enough to learn how money management can help you make more money. You'll be happier all around. When you feel good about your finances, you tend to be less stressed, get promoted faster, and enjoy life more.

So, who cares about personal financial matters? Everyone does! Personal finance is the most popular topic on the Internet. Google Trends shows that searches for "personal finances" have increased by 1,600% in the past four years.

People now use smartphones to track their money, compare prices and create wealth. You can read blogs such as this one, view videos on YouTube about personal finances, and listen to podcasts that discuss investing.

Bankrate.com reports that Americans spend four hours a days watching TV, listening, playing music, playing video games and surfing the web, as well as talking with their friends. It leaves just two hours each day to do everything else important.

Financial management will allow you to make the most of your financial knowledge.

What is the easiest passive source of income?

There are many options for making money online. Most of them take more time and effort than what you might expect. How do you find a way to earn more money?

The solution is to find what you enjoy, blogging, writing or selling. It is possible to make money from your passion.

For example, let's say you enjoy creating blog posts. Start a blog where you share helpful information on topics related to your niche. Then, when readers click on links within those articles, sign them up for emails or follow you on social media sites.

Affiliate marketing is a term that can be used to describe it. There are many resources available to help you get started. For example, here's a list of 101 Affiliate Marketing Tools, Tips & Resources.

Another option is to start a blog. Once again, you'll need to find a topic you enjoy teaching about. You can also make your site monetizable by creating ebooks, courses and videos.

Although there are many ways to make money online you can choose the easiest. You can make money online by building websites and blogs that offer useful information.

Once your website is built, you can promote it via social media sites such as Facebook, Twitter, LinkedIn and Pinterest. This is called content marketing, and it's a great method to drive traffic to your website.

Why is personal finance important?

Personal financial management is an essential skill for anyone who wants to succeed. We live in a world that is fraught with money and often face difficult decisions regarding how we spend our hard-earned money.

Why do we delay saving money? What is the best thing to do with our time and energy?

Yes and no. Yes, most people feel guilty saving money. Because the more money you earn the greater the opportunities to invest.

If you can keep your eyes on what is bigger, you will always be able spend your money wisely.

Controlling your emotions is key to financial success. When you focus on the negative aspects of your situation, you won't have any positive thoughts to support you.

It is possible to have unrealistic expectations of how much you will accumulate. This is because you aren't able to manage your finances effectively.

After mastering these skills, it's time to learn how to budget.

Budgeting is the act of setting aside a portion of your income each month towards future expenses. Planning will help you avoid unnecessary purchases and make sure you have enough money to pay your bills.

So now that you know how to allocate your resources effectively, you can begin to look forward to a brighter financial future.

How to create a passive income stream

To earn consistent earnings from the same source, it is important to understand why people make purchases.

Understanding their needs and wants is key. This requires you to be able connect with people and make sales to them.

Next, you need to know how to convert leads to sales. To retain happy customers, you need to be able to provide excellent customer service.

Even though it may seem counterintuitive, every product or service has its buyer. You can even design your entire business around that buyer if you know what they are.

It takes a lot of work to become a millionaire. A billionaire requires even more work. Why? Why?

You can then become a millionaire. Finally, you must become a billionaire. It is the same for becoming a billionaire.

How does one become a billionaire, you ask? It starts with being a millionaire. All you have to do in order achieve this is to make money.

Before you can start making money, however, you must get started. Let's now talk about how you can get started.

Statistics

- According to the company's website, people often earn $25 to $45 daily. (nerdwallet.com)

- 4 in 5 Americans (80%) say they put off financial decisions, and 35% of those delaying those decisions say it's because they feel overwhelmed at the thought of them. (nerdwallet.com)

- These websites say they will pay you up to 92% of the card's value. (nerdwallet.com)

- While 39% of Americans say they feel anxious when making financial decisions, according to the survey, 30% feel confident and 17% excited, suggesting it is possible to feel good when navigating your finances. (nerdwallet.com)

- Etsy boasted about 96 million active buyers and grossed over $13.5 billion in merchandise sales in 2021, according to data from Statista. (nerdwallet.com)

External Links

How To

How to Make Money While You Are Asleep

It is essential that you can learn to sleep while you are awake in order to be successful online. This means you need to be able do more than wait for someone else to click your link or purchase your product. Make money while you're sleeping.

You will need to develop an automated system that generates income without having to touch a single button. This requires you to master automation.

It would be helpful if you could become an expert at creating software systems that automatically perform tasks. By doing this, you can make money while you sleep. You can automate your job.

To find these opportunities, you should create a list with problems that you solve every day. Consider automating them.

Once you've done this, it's likely that you'll realize there are many passive income streams. The next step is to determine which option would be most lucrative.

A website builder, for instance, could be developed by a webmaster to automate the creation of websites. Perhaps you are a graphic artist and could use templates to automate the production logos.

If you have a business, you might be able to create software that allows you manage multiple clients simultaneously. There are hundreds of possibilities.

Automating anything is possible as long as your creativity can solve a problem. Automating is key to financial freedom.